-

Audit Industry, Services, Institutions

More security, more trust: Audit services for national and international business clients

-

Audit Financial Services

More security, more trust: Audit services for banks and other financial companies

-

Corporate Tax

National and international tax consulting and planning

-

Individual Tax

Individual Tax

-

Indirect Tax/VAT

Our services in the area of value-added tax

-

Transfer Pricing

Our transfer pricing services.

-

M&A Tax

Advice throughout the transaction and deal cycle

-

Tax Financial Services

Our tax services for financial service providers.

-

Advisory IT & Digitalisation

Generating security with IT.

-

Forensic Services

Nowadays, the investigation of criminal offences in companies increasingly involves digital data and entire IT systems.

-

Regulatory & Compliance Financial Services

Advisory services in financial market law and sustainable finance.

-

Mergers & Acquisitions / Transaction Services

Successfully handling transactions with good advice.

-

Legal Services

Experts in commercial law.

-

Trust Services

We are there for you.

-

Business Risk Services

Sustainable growth for your company.

-

IFRS Services

Die Rechnungslegung nach den International Financial Reporting Standards (IFRS) und die Finanzberichterstattung stehen ständig vor neuen Herausforderungen durch Gesetzgeber, Regulierungsbehörden und Gremien. Einige IFRS-Rechnungslegungsthemen sind so komplex, dass sie generell schwer zu handhaben sind.

-

Abacus

Grant Thornton Switzerland Liechtenstein has been an official sales partner of Abacus Business Software since 2020.

-

Accounting Services

We keep accounts for you.

-

Payroll Services

Leave your payroll accounting to us.

-

Real Estate Management

Leave the management of your real estate to us.

-

Apprentices

Career with an apprenticeship?!

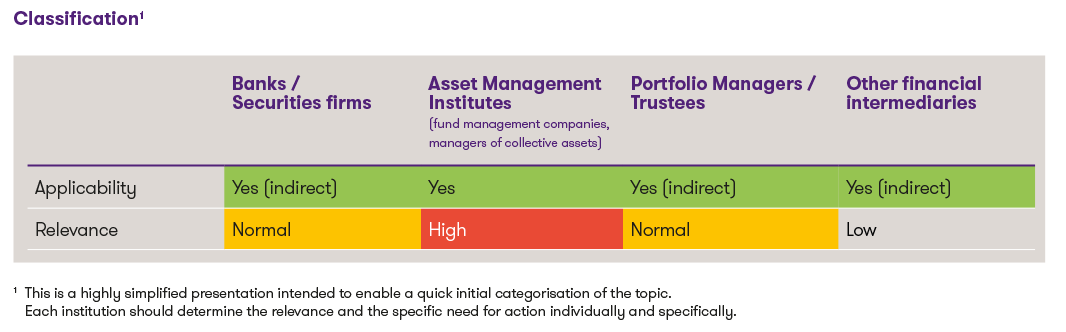

Einordnung der Neuerungen1

1 This is a highly simplified presentation, which should enable a quick initial classification of the topic. Each institution should determine the relevance and the specific need for action on an individual basis.

Increasing investments in private markets – background

More and more institutional and wealthy private investors are looking for alternatives to traditional forms of investment. Financial institutions that position themselves in this area can enjoy a competitive advantage. A study published recently with the assistance of the Asset Management Association Switzerland (AMAS) confirms this trend and emphasises the importance of a clear regulatory framework that is both aligned with international standards and innovative. From a Swiss regulatory perspective, the introduction of the Limited Qualified Investor Fund (L-QIF) exactly one year ago provided an important impetus in this direction. This new fund category creates more flexibility in the investment regulations and reduces the time to market for the launch of collective investment schemes. The L-QIF regulation particularly favours investments in private markets through this flexibility. This is also evident in the public directory of L-QIFs launched so far, which shows a focus on collective investment schemes in the private markets sector.

In this article, we examine private markets from a Swiss regulatory perspective and show who can operate such investment vehicles and which structures are best suited for this purpose.

Investments outside the stock exchange

Private markets generally refer to all asset classes that are traded outside of public capital markets. In contrast to public markets, such as equities or bonds, which are traded on exchanges, investments in private markets are made directly between investors and companies or through specialised fund structures.

In Swiss financial market regulation, private markets are generally classified as alternative investments and are not otherwise defined in more detail by law. However, the industry has established a classification into the following four areas:

- Private equity and venture capital: investments in unlisted companies with the aim of increasing their value through strategic and operational measures. This is done, for example, through growth financing, restructuring or management buyouts. Venture capital is generally seen as a subcategory of private equity and is characterised by a focus on companies in an early stage with high growth potential.

- Private debt/credit: Lending to companies outside of the traditional banking system. This form of financing offers companies flexible sources of capital and investors the opportunity to generate stable returns through interest income.

- Private infrastructure: Capital investments in long-term infrastructure projects such as energy supply, transport or telecommunications. These investments are characterised by stable and often inflation-protected returns.

- Private Real Estate: Investments in real estate, either directly or through specialised funds. The aim is to achieve long-term capital appreciation through rental income or property sales.

In addition to these four established areas, the asset class of so-called royalties has recently also been increasingly coming to the fore. These are shares in future revenues from licence fees and exploitation rights, such as payments made for the use of intellectual property or natural resources.

In summary, private markets are playing an increasingly important role for investors as they offer attractive returns, lower correlations to public markets and long-term growth opportunities. However, they usually require a longer capital commitment.

Regulatory framework

Investments in private markets are usually made through collective investment schemes in accordance with the Federal Act on Collective Investment Schemes (CISA) or foreign equivalents, as they require high minimum amounts and specialised management. In most cases, anyone who wishes to advise on, manage, distribute or administrate collective investment schemes in Switzerland requires a licence and must meet various regulatory requirements. The custodian bank, the fund management company, the asset manager and, depending on the case, the advisor and the distributor are subject to financial market supervision to varying degrees. The exact provisions depend on the specific set-up and the type of collective investment scheme and the target group (non-qualified or qualified investors). Typically, fund management companies, managers of collective assets, banks and securities firms are permitted to operate or manage collective investment schemes. In addition, conventional asset managers (Art. 17 FinIA), whose ongoing supervision is not carried out by FINMA but by supervisory organisations (SO), may also manage collective investment schemes below the so-called de minimis threshold. The amendments to the CISA introduced a year ago under the title ‘L-QIF’ offer, among other things, relief from the investment rules for funds that are limited to qualified investors. This significantly increases the opportunities for Swiss investment funds to invest in private markets.

In the area of investing and managing pension assets, investment foundations can be established that can, among other things, also form investment groups for private markets. In this case, the Collective Investment Schemes Act (CISA) does not provide the legal basis; instead, investment foundations are regulated by the Federal Law on Pension Schemes (BVG) and the Ordinance on Investment Foundations (ASV). Supervision is not carried out by FINMA, but by the Occupational Pension Supervisory Commission. If the pension assets are managed by an asset manager, this manager must in turn be supervised by FINMA or an AO.

Vehicles

The CISA offers various structures for private markets. Three of the most important investment vehicles are the contractual investment fund, the limited partnership for collective investments (LPCI) and the investment company with variable capital (SICAV):

- Contractual investment funds are the traditional and still most common form of Swiss collective investment schemes. Due to their limited flexibility, contractual investment funds are generally considered less suitable for private markets.

- The limited partnership is the Swiss variant of the limited partnership (LP), which is more common in the English-speaking world, and is specially designed for illiquid and long-term private markets investments. Its sole purpose is collective investment, which is particularly suitable for investments in real estate and infrastructure assets. It consists of a general partner with unlimited liability and limited partners with limited liability. It is a closed-ended investment vehicle, which means that investors have no right to redeem their units at any time. In return, the term of a limited partnership for collective investments is generally limited. A limited partnership for collective investments is only accessible to qualified investors and requires the approval of FINMA.

- The SICAV is a Swiss investment company with variable capital whose sole purpose is also collective investment. Since the capital and the number of shares of the SICAV are not determined in advance, it offers its investors flexible entry and exit options. Depending on its structure, the SICAV may also be offered to non-qualified investors. The SICAV is particularly suitable for liquid investments. Although exceptions to the right of redemption at any time may be granted, the high degree of investor flexibility can stand in the way of typical private markets investments, as the funds are invested in illiquid projects for longer periods of time.

For a year now, all three main forms of Swiss collective investment schemes can also be set up as L-QIFs and thus benefit from the associated regulatory relief. A glance at the current register of registered L-QIFs shows that L-QIFs have already been launched for all three categories (contractual, SICAV or limited partnership for collective investments), with most being structured as contractual investment funds. L-QIFs are characterised by the fact that they require neither a licence nor approval from FINMA and are also not supervised by FINMA. Only the licensing requirement for the institutions involved in the management of the L-QIF itself continues to apply. These simplifications make L-QIF particularly attractive for investments in private markets.

In addition, private market providers and investors can also access foreign investment funds. In Switzerland, Luxembourg and Irish fund structures are particularly dominant because they offer regulatory flexibility, tax efficiency and international recognition.

Alternative routes

In addition to the classic regulation by the CISA, there are alternative paths for private markets. In particular, investment companies with fixed capital in the form of joint-stock companies are exempt from the CISA, provided that only qualified shareholders can hold shares in them. This exemption may apply, for example, to direct investments by investors in a specific project or company. So-called investment clubs, which represent a joint investment by several investors in a specific project or company, are also possible. These regulatory exemptions offer exciting opportunities in simple and straightforward situations, enabling investments in private markets, but they are no longer suitable with increasing complexity, size and number of investors.

While direct investments were long reserved for institutional investors and high-net-worth individuals, new equity crowdfunding platforms are now enabling an ever-wider group of people to invest in private markets without traditional fund structures.

Conclusion

Private markets offer exciting investment opportunities, but are subject to strict regulatory requirements in Switzerland. The introduction of the L-QIF has given them more flexibility, which offers interesting opportunities in Switzerland, particularly for private markets. Careful planning and legal clarification are crucial to finding the right solution.

Would you like to find out more about how private markets can be integrated into your institution? We support financial service providers with comprehensive regulatory and compliance services in the areas of private markets, funds and collective investment schemes. This includes support during the FINMA licensing procedure and licence audits.