Markets in Crypto-Assets Regulation - Need for action for Swiss financial intermediaries

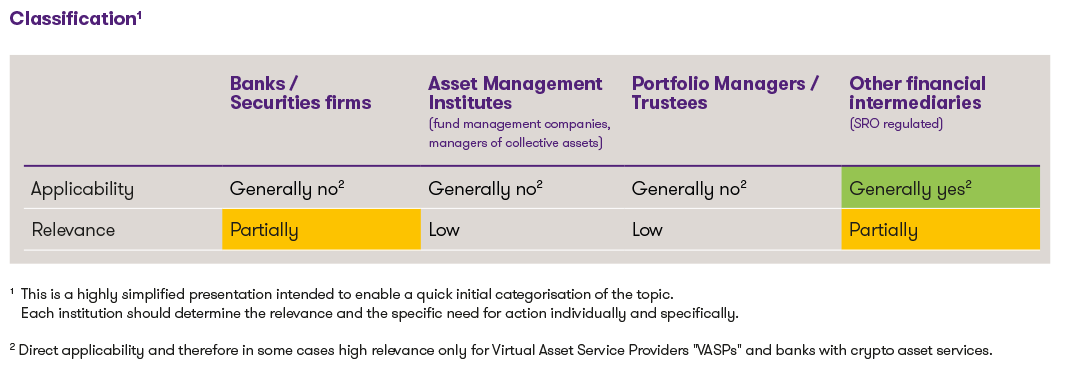

Classification 1

1 This is a highly simplified presentation intended to enable a quick initial categorisation of the topic. Each institution should determine the relevance and the specific need for action individually and specifically.

2 Direct applicability and therefore in some cases high relevance only for Virtual Asset Service Providers "VASPs" and banks with crypto asset services.

Scope and requirements

The scope of MiCA includes the providers of the following crypto-asset services («CASPs») to EU clients:

- Providing custody and administration of crypto assets on behalf of clients;

- Operation of a trading platform for crypto assets;

- Exchange of crypto assets for funds;

- Exchange of crypto assets for other crypto assets;

- Execution of orders for crypto assets on behalf of clients;

- Placing of crypto assets;

- Reception and transmission of orders for crypto assets on behalf of clients;

- Providing advice on crypto assets;

- Providing portfolio management on crypto assets;

- Providing transfer services for crypto assets on behalf of clients.

CASPs require authorisation from the national competent authority («NCA»). The requirements for such authorisation are, in particular, a registered office in the EU and the fulfilment of governance and capital requirements.

The scope of MiCA also extends to issuers of crypto assets in the EU. In particular, they must submit a so-called whitepaper with the prescribed content to the NCA at least 20 working days prior to publication and have it authorised if necessary. Depending on the type of crypto asset, issuers are also subject to an authorisation requirement. A distinction is made between the following types of crypto assets:

- E-money token («EMT»): A type of crypto-asset that purports to maintain a stable value by referencing the value of one official currency

- Asset-referenced token («ART»): a type of crypto-asset that is not an electronic money token and that purports to maintain a stable value by referencing another value or right or a combination thereof, including one or more official currencies

- Cryptocurrencies other than EMT and ART

EMTs can only be issued by authorised credit institutions or electronic money institutions. ARTs may only be issued by credit institutions or institutions that have a branch in the EU and are authorised by the NCA.

An EU authorisation as a CASP or issuer enables an institution to benefit from the EU passporting regime and to provide the offer or service throughout the EU.

However, the regulation only applies to crypto assets that are not regulated by existing financial services laws and therefore does not include traditional financial products with a crypto asset as the underlying or tokenised traditional financial instruments. Not yet in the scope of «MiCA 1.0» are, among others, Non-fungible crypto assets (so-called non-fungible tokens, «NFT») with exceptions, fully decentralised services (i.e. decentralised finance, «DEFI»), lending and borrowing with crypto assets, as well as the staking of crypto assets (other than ART and EMT).

Reverse solicitation

In principle, the regulation provides for an exemption from the requirement for EU authorisation in the case of reverse solicitation. However, the provision of crypto-asset services «at the own exclusive initiative of the client» must be verifiable and must be correspondingly well documented. As soon as a third-country firm acquires clients in the EU, reverse solicitation does not apply.

According to the recently published guidelines of the European Securities and Markets Authority (ESMA) , which are intended to ensure a common, uniform and consistent application of the reverse solicitation exemption, the exemption is to be interpreted narrowly. The term "solicitation" includes the promotion, advertising or offering of crypto-asset services or activities and it is irrelevant by what means the solicitation is carried out. Among others, ESMA lists the following means as examples: Internet commercials, banners, pop-ups and/or similar means on websites and social media, messaging platforms or sponsorship deals.

It is also irrelevant whether the acquisition is carried out by the third-country firm itself or by a person acting on its behalf (expressly by virtue of a contract or implicitly via an informal agreement) or who maintains close links with the third-country firm, which may include so-called influencers in particular. When assessing whether the contact was initiated exclusively by the client, the actual circumstances must always be taken into account; contractual agreements or disclaimers cannot be decisive if they are contradicted by the facts.

Furthermore, no new types of crypto-assets or crypto-asset services may be offered to an EU client who is served with crypto-asset services on its own exclusive initiative, but only those of the same type, whereby these must be related to the original transaction.

Financial intermediaries find helpful examples of circumstances in which a solicitation can be assumed in the Annex to the ESMA Guidelines.

Conclusion and outlook

Swiss institutions that provide crypto asset services should consider the scope and requirements of MiCA now at the latest, make a decision regarding serving the EU market and ensure the necessary compliance. Providers of crypto-asset services that have already provided their services under current law before 30 December 2024 must obtain authorisation by 1 July 2026 in order to continue providing their services to EU clients. It should be noted that the preparation of an application for authorisation and the authorisation procedure with the authorisation authorities will take some time, depending on the complexity of the application and the cooperation of the applicant in response to queries from the authorisation authorities. Serving the EU market on the basis of the reverse solicitation principle is likely to be very difficult to implement and reliance on this exemption provision should therefore be thoroughly clarified.