-

Audit Industry, Services, Institutions

More security, more trust: Audit services for national and international business clients

-

Audit Financial Services

More security, more trust: Audit services for banks and other financial companies

-

Corporate Tax

National and international tax consulting and planning

-

Individual Tax

Individual Tax

-

Indirect Tax/VAT

Our services in the area of value-added tax

-

Transfer Pricing

Our transfer pricing services.

-

M&A Tax

Advice throughout the transaction and deal cycle

-

Tax Financial Services

Our tax services for financial service providers.

-

Advisory IT & Digitalisation

Generating security with IT.

-

Forensic Services

Nowadays, the investigation of criminal offences in companies increasingly involves digital data and entire IT systems.

-

Regulatory & Compliance Financial Services

Advisory services in financial market law and sustainable finance.

-

Mergers & Acquisitions / Transaction Services

Successfully handling transactions with good advice.

-

Legal Services

Experts in commercial law.

-

Trust Services

We are there for you.

-

Business Risk Services

Sustainable growth for your company.

-

IFRS Services

Die Rechnungslegung nach den International Financial Reporting Standards (IFRS) und die Finanzberichterstattung stehen ständig vor neuen Herausforderungen durch Gesetzgeber, Regulierungsbehörden und Gremien. Einige IFRS-Rechnungslegungsthemen sind so komplex, dass sie generell schwer zu handhaben sind.

-

Abacus

Grant Thornton Switzerland Liechtenstein has been an official sales partner of Abacus Business Software since 2020.

-

Accounting Services

We keep accounts for you.

-

Payroll Services

Leave your payroll accounting to us.

-

Real Estate Management

Leave the management of your real estate to us.

-

Apprentices

Career with an apprenticeship?!

New FinSA circular - an overview of the most important challenges

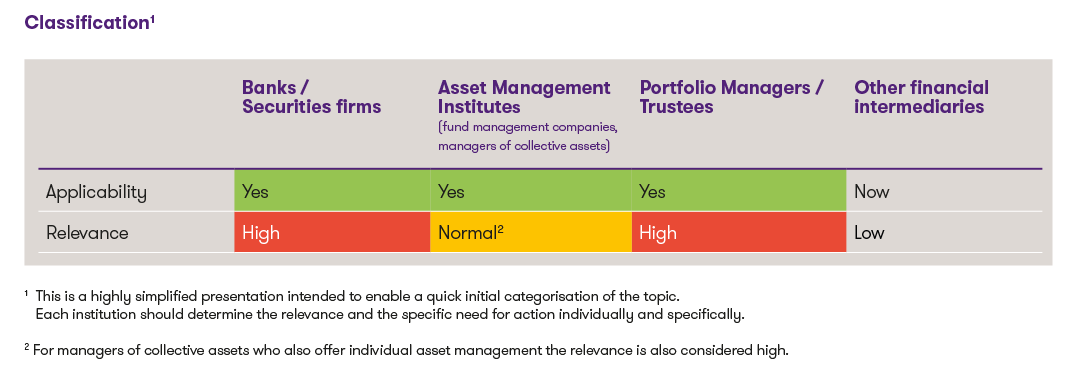

Classification of the innovations 1

1 This is a highly simplified presentation intended to enable a quick initial categorisation of the topic. Each institution should determine the relevance and the specific need for action individually and specifically.

2 For managers of collective assets who also offer individual asset management the relevance is also considered high.

Background

FINMA published the circular as a draft in May last year and then conducted a public consultation. On 22 November 2024, the final version of the circular was published and came into force on 1 January 2025, for certain parts with a transitional period until 30 June 2025. The circular is specifically intended to improve transparency regarding the type of financial service, the risks associated with financial instruments or financial services, conflicts of interest and compensation from third parties and retrocessions.

Please refer to our newsletters of 11 June 2024 and 3 December 2024 for the main contents and effects of the FinSA circular and the changes in the final circular compared to the draft.

The points where we have identified uncertainties in the implementation for many affected institutions are explained below.

Challenges to the implementation in practice

Cluster risks (margin no. 9-12)

The FinSA circular requires clients to be actively informed if cluster risks cannot be ruled out in the context of discretionary asset management or portfolio-based investment advice. The circular cites threshold values based on individual securities and issuers as examples or as a basic assumption on the part of FINMA for the existence of cluster risks. The explanatory report also mentions sectors, countries and currencies as criteria for cluster risks.

The circular does not require compliance with specific thresholds, but merely transparent information for clients on how financial service providers deal with cluster risks. This is also accompanied by the requirement that internal regulations for dealing with cluster risks should be created, which are appropriate to the business model and investment strategy of the financial services provider.

Various challenges are associated with this requirement:

- In addition to the regulatory component, the handling of cluster risks also contains a private law component (with appropriate risk diversification as part of the contractual due diligence obligations). Although the circular does not in principle preclude the investment of large parts of a portfolio in products of the same issuer or even in just one individual security (provided sufficient prior information is provided), financial service providers must also consider the appropriateness of such investment behavior from a private law perspective.

- While concentrations in collective investment schemes are generally not considered cluster risks under regulatory risk diversification rules by the circular, this does not apply to other instruments (namely AMCs), although these can also demonstrate appropriate diversification in themselves. On the other hand, the (constant) breakdown of such AMCs according to the asset classes they contain can be a difficult task to manage. Financial service providers must find a practicable solution for the assessment of such instruments in relation to cluster risks.

- For certain criteria (e.g. industries), it can sometimes be difficult to have sufficient data in sufficient granularity to be able to take them into account for the identification and avoidance of cluster risks.

- The duty to inform clients about cluster risks as set out in the circular contains also a monitoring duty for the financial services provider, as the ongoing compliance with the regulations and thresholds communicated to the client must be ensured. When defining internal rules, financial service providers must therefore also address the question of their verifiability and establish a suitable process with appropriate controls in the internal control system (ICS).

Appropriateness and suitability test (margin no. 14)

The circular states, among other things, that the financial service provider must enquire about the knowledge and experience of the client for each relevant asset class used in the financial service. This clarifies that the practice of merely recording the client's knowledge and experience in relation to the service as such, which is sometimes widespread in asset management and portfolio-based investment advice, is not sufficient.

For most financial service providers, an expansion of the previously used suitability questionnaire on customer knowledge and experience to include the common "standard asset classes" (equities, bonds, precious metals, etc.) should represent an appropriate implementation of the circular. Many companies probably already practised this before the existence of the FinSA circular.

However, financial service providers must not ignore the fact that the circular also requires the granularity of the questions to be adapted "to the complexity and risk profile of the investments and to the investment strategies that may be used in the financial service". Therefore, if a financial services provider focuses on certain "special" financial instruments in asset management or investment advice (e.g. certain structured products or forex transactions), the client's knowledge and experience in relation to these financial instruments should also be specifically enquired about.

Use of own financial instruments (margin no. 23-25)

If financial service providers use their own financial instruments as well as those of third parties, they must take appropriate measures to prevent any resulting conflicts of interest and inform clients of any unavoidable conflicts of interest.

Appropriate measures include, in particular, the implementation of a process for the selection of financial instruments based on industry-standard, objectified criteria. This can be challenging in some circumstances, as many asset managers have not yet endeavored to formulate their investment decision-making process in a general, abstract manner.

If certain thresholds are defined as a measure for the use of own financial instruments, it should be noted that these may not be higher than any thresholds defined as part of the regulation of cluster risks. This would represent a favoring of own financial instruments, which is likely to contradict the purpose of the circular.

Finally, it should be emphasized that the regulations on the use of own financial instruments also fundamentally affect financial services in the context of execution only. Here it may be appropriate to differentiate the internal regulations and client information so that the different structure of the various services is appropriately considered and safeguarded.

Retrocessions (margin no. 26-30)

The Circular has further specified the minimum information required for appropriate information on third-party compensation and made its granularity dependent, in particular, on the type of financial service. Accordingly, financial service providers will have to differentiate depending on the service as to which information must be disclosed in the contract itself and which may be provided as part of a general client information sheet. In addition, a contractually stipulated waiver of the surrender of retrocessions must now be emphasized visually, which will force some financial service providers with retro compensation models to adapt their contracts.

Repapering?

Many of the required measures can - depending on the setup already implemented at the institution - be implemented as part of expanded or additional client information and/or amendment of internal directives and documents. In contrast, the implementation of some changes (namely with regard to the content and presentation of information on retrocessions, as well as the determination of the client's knowledge and experience) will in many cases require the co-operation of the client.

Financial service providers need to carry out a precise analysis of the specific measures required based on their existing contracts. In doing so, they must find a way to harmonize the necessity of repaperings with the associated costs (for both the customer and the financial service provider).

In this context, special information letters and/or contract addenda may be a helpful transitional solution that can be used to comply with the regulations on the one hand and minimize the administrative effort on the other.

Conclusion and outlook

The new FinSA circular has some far-reaching implications on the practice of financial service providers. In particular, internal processes, contractual documents, documentation and controls must be revised promptly, whereby the specific and practicable implementation of the requirements may prove difficult in individual cases. Smaller financial service providers could face particular challenges in this regard and should consider the possibility of external support in order to ensure implementation in compliance with the regulations.

We will be happy to provide you with detailed information and support in implementing the new requirements.