-

Audit Industry, Services, Institutions

More security, more trust: Audit services for national and international business clients

-

Audit Financial Services

More security, more trust: Audit services for banks and other financial companies

-

Corporate Tax

National and international tax consulting and planning

-

Individual Tax

Individual Tax

-

Indirect Tax/VAT

Our services in the area of value-added tax

-

Transfer Pricing

Our transfer pricing services.

-

M&A Tax

Advice throughout the transaction and deal cycle

-

Tax Financial Services

Our tax services for financial service providers.

-

Advisory IT & Digitalisation

Generating security with IT.

-

Forensic Services

Nowadays, the investigation of criminal offences in companies increasingly involves digital data and entire IT systems.

-

Regulatory & Compliance Financial Services

Advisory services in financial market law and sustainable finance.

-

Mergers & Acquisitions / Transaction Services

Successfully handling transactions with good advice.

-

Legal Services

Experts in commercial law.

-

Trust Services

We are there for you.

-

Business Risk Services

Sustainable growth for your company.

-

IFRS Services

Die Rechnungslegung nach den International Financial Reporting Standards (IFRS) und die Finanzberichterstattung stehen ständig vor neuen Herausforderungen durch Gesetzgeber, Regulierungsbehörden und Gremien. Einige IFRS-Rechnungslegungsthemen sind so komplex, dass sie generell schwer zu handhaben sind.

-

Abacus

Grant Thornton Switzerland Liechtenstein has been an official sales partner of Abacus Business Software since 2020.

-

Accounting Services

We keep accounts for you.

-

Payroll Services

Leave your payroll accounting to us.

-

Real Estate Management

Leave the management of your real estate to us.

-

Apprentices

Career with an apprenticeship?!

FINMA brings new FinSA circular into force - Overview of the most important changes

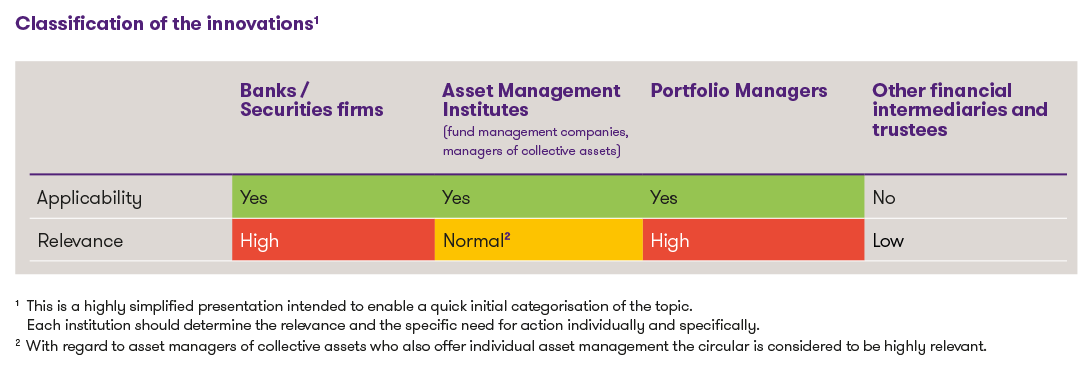

Classification of the innovations1

1 This is a highly simplified presentation intended to enable a quick initial categorisation of the topic. Each institution should determine the relevance and the specific need for action individually and specifically.

2 With regard to asset managers of collective assets who also offer individual asset management the circular is considered to be highly relevant.

Background

The Swiss Financial Market Supervisory Authority (FINMA) has finalised and published the circular on rules of conduct under the Financial Services Act (FinSA). This will enter into force on 1 January 2025 and aims to create uniform standards for the provision of information and support to clients in the financial services sector. There is a transitional period until 30 June 2025 for the implementation of certain requirements. The circular was discussed intensively during the consultation and criticised by industry representatives. FINMA has taken up various points from the consultation and amended them in the final version but has retained all the essential core content of the draft.

Changes in the final circular compared to the draft

Although numerous participants in the consultation generally called for the circular to be abandoned, FINMA adhered to the decree. Overall, relatively few changes were made to the final version of the circular compared to the draft. With regard to the main contents and effects of the FinSA Circular, we therefore generally refer to our newsletter of 11 June 2024.

The points where FINMA has made significant changes based on feedback from the consultation are explained below:

-

Appropriateness and suitability test (margin no. 14): When recommending financial products or services, the provider must take into account the client's knowledge, experience, financial circumstances and investment objectives. Margin no. 14 of the new circular specifies that the financial service provider must enquire about the client's knowledge and experience for each relevant investment category that applies to the financial service. This passage caused a great deal of discussion in the industry during the consultation. Some feared the introduction of "product suitability" for discretionary asset management mandates, as the suitability of the relevant financial instrument would now have to be proven for each individual transaction. FINMA has addressed these concerns and reworded margin no. 14 to take account of the differences in suitability for asset management, portfolio-related investment advice and transaction-related investment advice. In the case of asset management, appropriateness and suitability will therefore continue to be ensured taking into account the characteristics of the investment strategy and the types of financial instruments used, but a separate suitability test at the level of the individual financial instrument is not necessarily required for each transaction executed.

-

Conflicts of interest / use of own financial instruments (margin nos. 23-25): The regulations on the identification and management of conflicts of interest are further specified. Financial service providers must have appropriate organisational measures in place to identify and avoid conflicts of interest or, if unavoidable, to make them transparent and manage them. One adjustment to the final circular compared to the draft is that only "unavoidable" conflicts of interest must be disclosed when using own financial instruments. In any case, according to the wording of the final circular, the duty to provide information includes informing clients in advance whether the market offer taken into account comprises (a) only own, (b) own and third-party or (c) only third-party financial instruments. The final circular also adds that own financial instruments may not be promoted through incentives in the remuneration system.

-

Placement of financial instruments (margin no. 3): Margin no. 3 of the new FinSA circular restricts the scope of application of the exemption provision of Art. 3 para. 3 let. b FinSO. According to this exception, the placement of financial instruments (e.g. as part of corporate finance services) is not considered a financial service within the meaning of FinSA. According to the new FinSA circular, this exception only applies to the upstream relationship between financial service providers and companies that finance themselves via the capital market and their shareholders. However, if a service for the placement of financial instruments takes place directly between the financial service provider and the (end)client in the latter's capacity as an investor, the placement of financial instruments may constitute a financial service.

- Information on contracts for difference (margin no. 5-8): Contracts for difference are derivative financial instruments with a specific risk structure. FINMA assumes that more clients tend to lose money with contracts for differences than make profits. The circular therefore sets out specific risk disclosure obligations in the area of contracts for differences. Despite criticism from the industry, the final version not only retained the specific risk disclosure obligations, but even extended them - also with reference to similar obligations in the EU. In addition to prior information on any margin calls, potentially unlimited risk of loss, leverage effect, how the margin works and other risks, the client must now also be informed on a quarterly basis. This information obligation includes the proportion (in %) of private clients who (1) have lost money with contracts for difference in the last 12 months, (2) have suffered a total loss of their margin and (3) have had to pay a negative balance after closing their positions.

Unchanged key contents of the circular

- Bulk risks (margin nos. 9-12): The FinSA circular introduces new information obligations on the topic of cluster risks. Despite criticism during the consultation process, this remains unchanged in the final circular. Bulk risks arise when there is a concentration of risks in a few positions or issuers in a client's portfolio. In addition to risk concentrations in individual securities and asset classes, cluster risks also include, in particular, concentrations in the same issuers and correlating sectors, countries and currencies. Financial service providers must take appropriate measures to recognise, assess and manage such risks. This includes the regular review and diversification of portfolios to ensure that no excessive risks arise from clustering. The circular requires clients to be actively informed about cluster risks that are unusual for the market (from 10% in individual securities or from 20% for individual issuers). In the case of professional clients who contractually exempt the financial services provider from the obligation to provide information, information on cluster risks is also generally not required.

- Retrocessions (margin nos. 26-30): Another important aspect of the FinSA circular concerns the topic of retrocessions, where the current requirements are specified in both formal and material terms, also taking into account the case law of the Federal Supreme Court. In particular, the circular requires that information on retrocessions must be visually emphasised in form contracts and must be physically available or easy to find electronically. Despite extensive criticism during the consultation process, the new requirements on retrocessions were retained unchanged in the final circular. Financial service providers that use remuneration models with retrocessions must therefore review their internal processes and the contracts used and adapt them if necessary.

Transitional provision (margin no. 31)

In response to the comments of numerous industry representatives, FINMA has introduced a 6-month transitional period until 30 June 2025 with regard to the following provisions of the new circular:

- Obligation to inform the customer on a quarterly basis for contracts for differences;

- Obligation to provide information on cluster risks or concentrations of 10% or more in individual securities and 20% or more in individual issuers;

- Duty to provide information and deal with conflicts of interest in connection with own and third-party financial instruments;

- Obligation to provide information on third-party compensation/retrocessions in form contracts by means of visual highlighting.

Conclusion and outlook

The new FinSA circular has implications for the practice of financial service providers and comes into force in around a month. In particular, internal processes, contractual documents, documentation and controls must be revised promptly in order to fulfil the new requirements. Smaller financial service providers could face particular challenges in this regard and should consider the possibility of external support to ensure implementation in compliance with the regulations.

We will be happy to provide you with detailed information and support in implementing the new requirements.