-

Audit Industry, Services, Institutions

More security, more trust: Audit services for national and international business clients

-

Audit Financial Services

More security, more trust: Audit services for banks and other financial companies

-

Corporate Tax

National and international tax consulting and planning

-

Individual Tax

Individual Tax

-

Indirect Tax/VAT

Our services in the area of value-added tax

-

Transfer Pricing

Our transfer pricing services.

-

M&A Tax

Advice throughout the transaction and deal cycle

-

Tax Financial Services

Our tax services for financial service providers.

-

Advisory IT & Digitalisation

Generating security with IT.

-

Forensic Services

Nowadays, the investigation of criminal offences in companies increasingly involves digital data and entire IT systems.

-

Regulatory & Compliance Financial Services

Advisory services in financial market law and sustainable finance.

-

Mergers & Acquisitions / Transaction Services

Successfully handling transactions with good advice.

-

Legal Services

Experts in commercial law.

-

Trust Services

We are there for you.

-

Business Risk Services

Sustainable growth for your company.

-

IFRS Services

Die Rechnungslegung nach den International Financial Reporting Standards (IFRS) und die Finanzberichterstattung stehen ständig vor neuen Herausforderungen durch Gesetzgeber, Regulierungsbehörden und Gremien. Einige IFRS-Rechnungslegungsthemen sind so komplex, dass sie generell schwer zu handhaben sind.

-

Abacus

Grant Thornton Switzerland Liechtenstein has been an official sales partner of Abacus Business Software since 2020.

-

Accounting Services

We keep accounts for you.

-

Payroll Services

Leave your payroll accounting to us.

-

Real Estate Management

Leave the management of your real estate to us.

-

Apprentices

Career with an apprenticeship?!

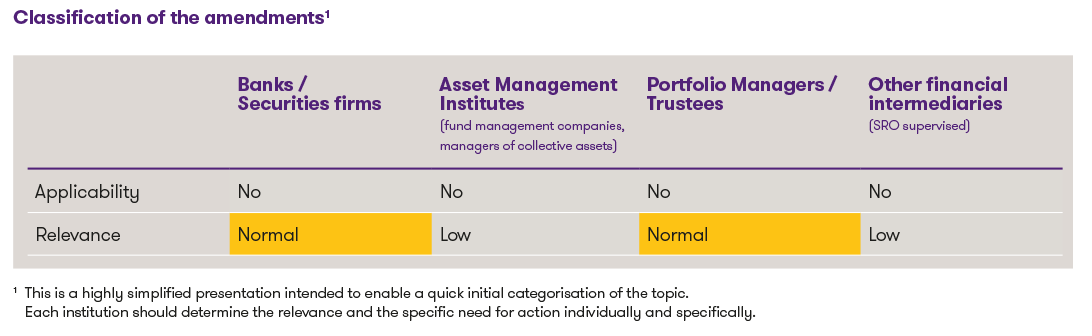

Classification of the innovations1

1 This is a highly simplified presentation intended to enable a quick initial categorisation of the topic. Each institution should determine the relevance and the specific need for action individually and specifically.

Money laundering package to strengthen EU regulations

The new package consists of the following components. However, no agreement has yet been reached on the changes in connection with the ordinance on the revision of the Transfer of Funds Regulation ("TFR") and the date of entry into force cannot yet be estimated.

- Directive on Anti-money laundering mechanisms ("AMLD"). It contains provisions on the organisation of the institutional system. It regulates, in particular, the tasks and powers of the supervisory authorities and the Financial Intelligence Units (FIU).

- Regulation on the Private Sector's Obligation to Combat Money Laundering ("AMLR"). This ordinance regulates the relevant due diligence obligations of those subject to it. The aim of the new ordinance is to standardise and clarify the applicable regulations.

- Regulation establishing a new EU Anti-money laundering authority ("AMLA"). It primarily regulates the tasks and powers of the new authority to be established.

- Regulation on the revision of the Regulation on Transfers of Funds ("TFR"). The regulations will be extended to crypto assets with the aim of making crypto asset transfers more transparent and traceable.

The new provisions of the AMLD, AMLR and AMLA are of high importance.

Regulation on the obligation of the private sector to combat money laundering ("AMLR")

The most significant change is probably the inclusion of additional legal entities in the list of persons subject to Anti-money laundering legislation. For example, all providers of crypto services must now apply due diligence obligations for their customers as soon as transactions with a value of EUR 1,000 or more are carried out. Furthermore, dealers of luxury goods (including precious metals and gemstone dealers, jewellers, goldsmiths, but also dealers of luxury cars, aircraft, yachts, works of art, etc.) will also be subject to due diligence and reporting obligations in future. In addition, professional football clubs and agents must apply due diligence obligations in certain cases from 2029 (an extended transitional period applies here) and report suspicious transactions to the FIU.

The EU-wide maximum limit of EUR 10,000 for cash payments is also far-reaching. In future, people who want to pay EUR 10,000 or more in cash will have to identify themselves and prove where the money comes from. On the other hand, merchants are obliged to keep a record of the information received.

In the case of very wealthy persons (so-called ultra-rich individuals with a net worth ≥ EUR 50 million), the enhanced due diligence obligations apply directly.

Unlike in Switzerland, a register of beneficial owners is already kept in the EU (we already reported on this topic in February 2024). In the future, certain foreign legal entities will also be required to be entered in the register of beneficial owners. This is the case if they actually control the ownership of a legal entity or benefit from the fact that the title or ownership is in a different name. Beneficial ownership is therefore based on two components: ownership and control. The 25% threshold is still decisive. In addition to those previously authorised to access the register (e.g. supervisory and other authorities), representatives of the public (such as the press) will now also have access to the register, provided they have a legitimate interest.

Regulation establishing a new EU Anti-money laundering authority ("AMLA")

The new authority will be based in Frankfurt and is expected to commence operations in mid-2025. The main tasks of the new authority will be the direct supervision of some high-risk institutions (e.g. providers of crypto services) and the coordination of the FIUs. The new authority will also be authorised to impose sanctions and fines in the event of serious violations.

Directive on Anti-money laundering mechanisms ("AMLD")

The powers of the FIUs, i.e. the money laundering reporting centres, will be expanded. In order to properly analyse and detect cases and suspend suspicious transactions, they will be, amongs other rights, granted direct access to financial, administrative and law enforcement information.

Conclusion and schedule

At the beginning of 2024, the European Parliament and the Council reached an agreement on part of the package of legislative proposals presented in 2021 to strengthen EU rules on combating money laundering and terrorist financing. The final compromise version is currently being approved by the Committee of Permanent Representatives of the Member States. Following publication of the decrees in the Official Journal of the EU, the laws will formally enter into force. The two regulations ("AMLR" and "AMLA") are in principle directly applicable to EU member states. For the Directive ("AMLD"), the Member States have 3 years to transpose the provisions into their national legal systems. The substantive entry into force of the directive can therefore be expected for Q1 2027. However, a postponement is quite possible. The regulations will enter into force automatically without having to be incorporated into the respective national law.

As a non-EU member, Switzerland is not directly affected by the changes to the EU's money laundering counter measures. However, legal developments in the EU have a significant influence on Swiss legislation, especially as combating money laundering is also high on the list of priorities in Switzerland. It is therefore to be expected that - in particular the adjustments in the AMLR - will sooner or later find their way into Swiss legislation in a similar form.